They say nothing is certain but death and taxes, but some people think they can avoid at least one of these.

This post is about the people who call themselves sovereignty advocates, state nationals, private men and women, etc., and whom others may call sovereign citizens, tax protestors, tax scammers, etc. In my post The conspiracy theory that revolves around wordplay, I described how the sovereign citizen movement uses idiosyncratic definitions of many words, specifically to reinterpret laws in ways that benefit them. For example, sovereign citizens frequently insist when pulled over that they are not driving but rather traveling, and thus aren’t required to have a driver’s license or follow traffic laws.

A central part of the sovereign citizen theory is that they are not US citizens. A common way this is supported is by pointing to a statute in the United States Code, 8 USC § 1101(a)(36), which says:

The term “State” includes the District of Columbia, Puerto Rico, Guam, the Virgin Islands of the United States, and the Commonwealth of the Northern Mariana Islands.

According to the sovereign citizen argument, the word “includes” here means “includes only“, as in this definition sneakily defines the United States as consisting exclusively of these territories and district. This is important because it vastly limits the jurisdiction of the federal government. And since US citizens are defined (in part) as people born in the US, anyone born in the 50 states is not a citizen. Many (incorrect) interpretations of statutes hinge upon this understanding of “includes”.

The argument

So, what justification is given for this unusual definition? Well, the sovereign citizen movement is not ideologically unified, so there may be many, but in this post I will look in depth at a typical exemplar. The “sister sites” Sovereign Education Defense Ministry (SEDM) and Family Guardian have extensive resources for learning about issues like this, mostly in the form of long pdf documents. I will be referring primarily to their document The Great IRS Hoax: Why We Don’t Owe Income Tax (version 4.54), a nearly 3,000-page long manifesto and treatise on many important sovereign citizen issues. Strangely, the document says on the cover that it was written by the “Department of the Treasury, Tax Research Division”, but it later clarifies that it was written by the creator(s) of SEDM/Family Guardian with the help of several people contributing ideas or parts of sections (p. 15, Preface). From here on out I’ll just refer to the author(s) of The Great IRS Hoax as SEDM. Also, the document is conveniently organized into numbered sections and subsections, so I will include both the page number of the pdf and the section number in my references. This should help if future revisions rearrange things.

While this document covers many topics, we are only concerned here with the meaning of “include”. This is addressed at varying levels of detail in a few different sections. See p. 24, Preface; p. 485, §3.6.2; pp. 547-549, §3.9.1.8; pp. 1623-1625, §5.2.13.2, and pp. 2685-2689, §5.10.6. The points we will discuss are as follows:

- Four dictionary definitions of “include”

- The “void for vagueness” doctrine and the legal principles of expressio unius, exclusio alterius and ejusdem generis

- The cases Gould v. Gould, Powers v. Charron, United States v. Love, and others

- The wording of 26 USC § 7701(c), 26 USC § 61, and other statutes

Let’s now take a look at the evidence SEDM provides, starting with this definition for “include”.

First definition

includes- as defined in Treasury Decision 3980, Vol. 29, January-December, 1927, pgs. 64 and 65 means the following:

“(1) To comprise, comprehend, or embrace…(2) To enclose within; contain; confine…But granting that the word ‘including’ is a term of enlargement, it is clear that it only performs that office by introducing the specific elements constituting the enlargement. It thus, and thus only, enlarges the otherwise more limited, preceding general language…The word ‘including’ is obviously used in the sense of its synonyms, comprising; comprehending; embracing.”

(p. 24, Preface)

We start off on the right foot. There is no problem with this definition. However, SEDM is interpreting this definition in a specific way. SEDM is concerned with the idea of “enlargement” and “limitation”. The concern is that Congress uses “including” to make the definition more vague by introducing the idea that there are additional, unnamed items. Thus Congress enlarges the definition to contain potentially anything. This is the perceived problem that SEDM wants to address through defining “include”. The definition given correctly states that “including” only (possibly) enlarges a definition by the particular items listed. The confusion is that this is not a distinction that is being made because of the kind of “enlargement” SEDM has in mind.

This is the situation the definition is talking about: often, when we have a definition that “includes” specific things, they are merely examples. However, there are some cases in which “includes” or “including” is used to clarify that something is not excluded by the definition. In other words, the normal understanding of the term may not include the item, so to make it unambiguous we explicitly state that the item is included. This is the “enlargement” in question. For example, one might say something like, “all rocks, including ice, …” because the everyday conception of what a rock is does not include ice. The same language without “including” would be more limited and more general. “Including” makes the definition less vague.

SEDM also calls attention to synonyms of “include” like comprise, comprehend, embrace, enclose, contain, confine, (and, later on p. 548, §3.9.1.8:) admit, receive, circumscribe, compose, incorporate, encompass, take in, attain, shut up, inclose, and involve. The key I think is this idea of closure implying limitation. However, this is like reinforcing the walls when the enemy is already inside. “Including” requires the strict enclosure of the listed items, but has nothing to say about what else is contained. Some synonyms, it should be noted, are not generally interchangeable with “include”. A synonym is not a word with the exact same meaning.

Expressio unius, exclusio alterius

The term “includes” is a term of limitation and not enlargement. Where it is used, it prescribes all of the things or classes of things to which the statute pertains. All other possible objects of the statute are thereby excluded, by implication.

“expressio unius, exclusio alterius”—if one or more items is specifically listed, omitted items are purposely excluded. Becker v. United States, 451 U.S. 1306 (1981)

(p. 485, §3.6.2, emphasis in the original)

To clarify, only the phrase in Latin comes from Becker v. United States. The rest is SEDM’s interpretation and assertion. Let’s see the context:

The language of Rule 62(d) seems clear, and the enumerated exceptions do not include tax summons enforcement proceedings. Expressio unius est exclusio alterius. Contrary to the Government’s assertion, an order enforcing an IRS summons is not the “equivalent” of a mandatory injunction-and hence within the exceptions of Rule 62(d)-simply because the coercive power of the court is invoked.

The question at hand is whether an order enforcing an IRS summons falls under the exceptions to the automatic stay rule, which would grant a 30-day stay on proceedings to enforce it. Here is the relevant list of exceptions:

Injunction Pending an Appeal. While an appeal is pending from an interlocutory order or final judgment that grants, continues, modifies, refuses, dissolves, or refuses to dissolve or modify an injunction, the court may suspend, modify, restore, or grant an injunction on terms for bond or other terms that secure the opposing party’s rights. If the judgment appealed from is rendered by a statutory three-judge district court, the order must be made either:

(1) by that court sitting in open session; or

(2) by the assent of all its judges, as evidenced by their signatures.

Notice that this does not use the word “include” in any form, but rather lists things with “or”. This implies that what the court meant by expressio unius, exclusio alterius that when items are listed with “or”, the list is comprehensive, and it cannot apply to unlisted items. It does not say anything about “include”.

Second definition

As you probably know, Black’s Law Dictionary is the Bible of legal definitions. See what it says:

“Include. (Lat. Inclaudere, to shut in. keep within.) To confine within, hold as an inclosure. Take in, attain, shut up, contain, inclose, comprise, comprehend, embrace, involve. Term may, according to context, express an enlargement and have the meaning of and or in addition to, or merely specify a particular thing already included within general words theretofore used. “Including” within statute is interpreted as a word of enlargement or of illustrative application as well as a word of limitation. Premier Products Co. v. Cameron, 240 Or. 123, 400 P.2d. 227, 228.”

[Black’s Law Dictionary, Sixth Edition, p. 763]

In other words, according to Black, when INCLUDE is used it expands to take in all of the items stipulated or listed, but is then limited to them!(p. 548, §3.9.1.8)

In general, this is in line with what I said about the first definition above. The key for SEDM in this definition is the last sentence, specifically as well as a word of limitation. It turns out that almost this entire sentence comes word-for-word from Premier Products Co. v. Cameron.

The statute requires employers to pay unemployment taxes for all employees unless exempted by statute. ORS 657.087 provides:

“`Employment’ does not include service performed by individals [sic] soliciting contracts for home improvements including roofing, siding and alterations of private homes to the extent that the remuneration for such services primarily consists of commissions or a share of the profit realized on each contract.”

On oral argument the attorney for the Commissioner admitted that if it were not for the phrase, “including roofing, * * *,” petitioner’s employees would be soliciting contracts for “home improvements.” The Commissioner’s contention is that “including” is a word of limitation; that the general phrase, “home improvements,” is limited to only certain kinds of “home improvements,” namely, “roofing, siding and alterations.”

1-3. This is the kind of statutory interpretation question in which a court need not pay deference to an administrative interpretation: Rogers Const. Co. v. Hill, 235 Or 352, 357, 384 P2d 219 (1963). No plausible reason has been given for distinguishing between salesmen of such home improvements as roofs and salesmen of such home improvements as windows. The known legislative history contains no indication that such a distinction was intended. “Including” can and has been interpreted as a word of enlargement, or of illustrative application, as well as a word of limitation: Arnold v. Arnold, 193 Or 490, 502, 237 P2d 963, 239 P2d 595 (1952); Federal Land Bank v. Bismark Lumber Co., 314 US 95, 62 S Ct 1, 86 L ed 65 (1941). How it is interpreted depends upon several factors, context, subject matter, possible legislative intention, etc.

We construe the statute as not being limited to sellers of roofing, siding and alterations, but rather, to include sellers of custom storm doors, windows, and patio covers.”

(Premier Products Co. v. Cameron (1965), emphasis added)

So this decision specifically applies a statute in a situation not listed after the word “including”, contrary to SEDM’s argument. It does, however, acknowledge that “including” can be a term of limitation, and cites two additional cases, Arnold v. Arnold and Federal Land Bank v. Bismark Lumber Co.

Arnold v. Arnold concerns the jurisdiction of a court of probate over a certain issue. It says the following, beginning with quoting the statute:

“Section 11. In any cause, matter or proceeding over which by existing laws the circuit court of such judicial district has jurisdiction, the procedure and practice shall be governed by existing laws applicable to such cause, matter or proceeding without change, and there also hereby is conferred upon, and vested in, such circuit court full, complete, general and exclusive jurisdiction, authority and power in equity, in the first instance, in all matters whatever pertaining to a court of probate, including the construing of, and declaration of rights under, wills and codicils, and therein the determining of question of title to real, personal or mixed properties; …

In our opinion, the provisions of § 11 were intended not only to enumerate, but also to define, the powers of the Circuit Court for Multnomah County when sitting in probate.

(Arnold v. Arnold (1952) , emphasis added)

The decision explains that, if the clause ended with “all matters whatever pertaining to a court of probate”, it would have been too vague and would have given the judiciary the responsibility to define it more clearly. The purpose of “including” here is to clarify what kinds of things a court of probate has jurisdiction over. It makes it more specific and therefore more limited. Contrary to SEDM’s argument, it does not actually limit the court’s jurisdiction to only those things listed. Rather, the listed examples serve to identify the category of disputes that a court of probate can rule on, thereby (by implication) excluding other categories.

More strikingly, Federal Land Bank v. Bismark Lumber Co. explicitly contradicts SEDM.

The unqualified term “taxation” used in § 26 clearly encompasses within its scope a sales tax such as the instant one, and this conclusion is confirmed by the structure of the section. In reaching an opposite conclusion, the court below ignored the plain language, “That every Federal land bank . . . shall be exempt from Federal, State, municipal, and local taxation,” and seized upon the phrase, “including the capital and reserve or surplus therein and the income derived therefrom,” as delimiting the scope of the exemption. The protection of § 26 cannot thus be frittered away. We recently had occasion, under other circumstances, to point out that the term “including” is not one of all-embracing definition, but connotes simply an illustrative application of the general principle.

(Federal Land Bank v. Bismark Lumber Co. (1941), emphasis added)

In the case of SEDM and 8 USC § 1101, they are ignoring the plain language, “The term ‘United States’, except as otherwise specifically herein provided, when used in a geographical sense, means the continental United States, Alaska, Hawaii, Puerto Rico, Guam, the Virgin Islands of the United States, and the Commonwealth of the Northern Mariana Islands” (emphasis added) and seizing upon the phrase “includes the District of Columbia, Puerto Rico, Guam, the Virgin Islands of the United States, and the Commonwealth of the Northern Mariana Islands.”

Tracing our way backwards, we see that the only “limitation” in Premier Products Co. v. Cameron, which is the source for “limitation” in Black’s Law Dictionary, which is what SEDM’s argument relies on, comes from Arnold v. Arnold, which does not support SEDM’s conclusion.

Third definition

Bouvier’s Law Dictionary (written by the U.S. Supreme Court Justice with the same name) has the following definitions:

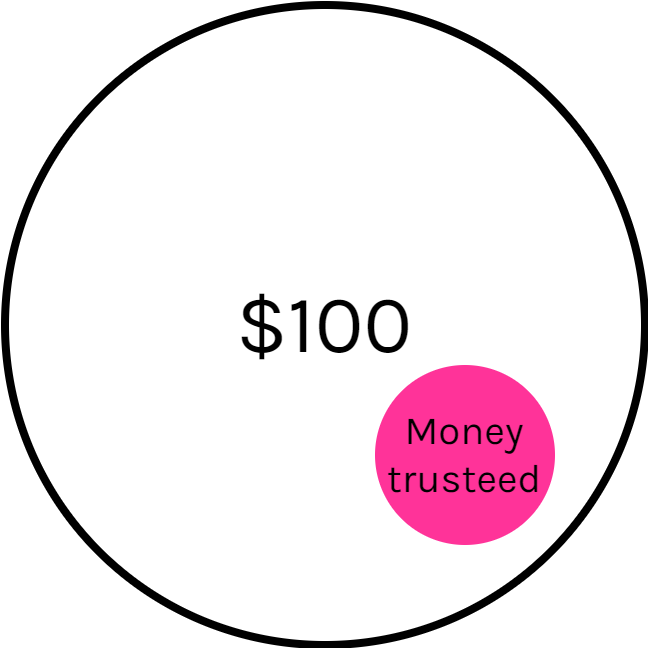

“INCLUDE (Lat. in claudere to shut in, keep within). In a legacy of ‘one hundred dollars including money trusted [sic]’ at a bank, it was held that the word ‘including’ extended only to a gift of one hundred dollars; 132 Mass. 218…”

“INCLUDING. The words ‘and including’ following a description do not necessarily mean ‘in addition to,’ but may refer to a part of the thing described. 221 U.S. 425.”

[Bouvier’s Law Dictionary, Justice John Bouvier, 1856; …](p. 548, §3.9.1.8)

A minor point of clarification is that Bouvier’s Law Dictionary says “trusteed” here, not “trusted”.

Again, the problem here is not with the definition itself, but with SEDM’s interpretation. For SEDM to be correct, the definition of “include” would need to say that the $100 consists solely and exclusively of money trusteed at the bank. The clarification the definition is making here is that including doesn’t mean in addition to, i.e. the $100 extends beyond money trusteed at the bank but is not in addition to money trusteed at the bank. The fact that this is what the definition means is reiterated in the definition of “including”.

Fourth definition

And, in everyday life, the meaning of these words is a RESTRICTIVE one, not an EXPANSIVE one.

Read the American College Dictionary:

“include, v.f.;-cluded, -cluding. 1. to contain, embrace, or comprise, as a whole does parts or any part or element.”

“included, adj. 1. enclosed; embraced; comprised. 2. But. [sic] not projecting beyond the mouth of the corolla, as stamens or a style.”

Note that here, even the Botanical meaning is a confining use!

(p. 548, §3.9.1.8)

The only new piece of information here is the “botanical meaning”. This is not a “confining use” as SEDM would understand it. This is saying that the corolla does extend beyond the stamens or style. It extends an unspecified (expansive) distance. A better match would be if “included” meant extending precisely to the mouth of the corolla. As with the first definition, SEDM is getting the “enclosing” part backwards.

Gould v. Gould

[T]he U.S. Supreme Court put a nail in the coffin of the expansive use of the word “includes” when it said the following:

“In the interpretation of statutes levying taxes, it is THE EXTABLISHED RULE NOT TO EXTEND their provisions, by implication, BEYOND THE CLEAR IMPORT OF THE LANGUAGE USED, OR TO ENLARGE their operations SO AS TO EMBRACE MATTERS NOT SPECIFICALLY POINTED OUT”.

[Gould v. Gould, 245 U.S. 151](p. 549, §3.9.1.8)

For some reason this quote has been slightly modified. For comparison, here is the actual relevant text of the case:

In the interpretation of taxing statutes it is the established rule not to extend their provisions, by implication, beyond the clear import of the language used, or to enlarge their operations so as to embrace matters not specifically pointed out.

It is, beyond all reasonable doubt, the clear import of the language used in 8 USC § 1101 that the United States is defined in such a way that someone born in one of the 50 states is a US citizen. Evidence for this is that virtually everyone interprets the language to mean this and has no confusion about it. If the clear import was to the contrary, it would not be necessary for SEDM to explain at length the “true meaning”.

Statutory definition and “but not limited to”

The Internal Revenue Service wants you to believe that the Tax Code covers everything that is listed in the Code, and can be expanded to involve anything else they may decide upon at any later date without the need to rewrite the law! Look at the “definition” written in the Internal Revenue Code:

“Sec. 7701(c) INCLUDES AND INCLUDING. – The terms ‘include’ and ‘including’ when used in a definition contained in this title shall not be deemed to exclude other things otherwise within the meaning of the term defined.”

This would, at first glance, seem to say that these words are used in the Code in an expansive way, not a limiting way. (However, if you carefully analyze this “definition,” you discover that it is a classic example of “double-talk.” It really doesn’t say ANYTHING!)(p. 547, §3.9.1.8, emphasis in the original)

26 USC § 7701(c) is really damning to SEDM’s argument. They offer two responses here, first that the definition is “double-talk” and second that it’s contradicted by 26 USC § 61. We’ll address each in turn.

“Double-talk” or more commonly doublespeak involves obfuscation through euphemism and ambiguity. A commonly given example of doublespeak is referring to used cars as “pre-owned”. Let’s break the definition down in detail and see how clear it is.

The terms “includes” and “including” …

I don’t think there is any ambiguity here. We are talking about two specific words, specifically two forms of the verb to include. This is saying that what follows applies to both “includes” and “including”.

… when used in a definition contained in this title …

“This title” is Title 26 of the U.S. Code. 26 USC Chapter 79 under Subtitle F is “definitions” (though it is possible there are definitions that exist elsewhere in Title 26). For example, 26 USC § 7701(c) is a definition contained in this title. A term being used in a definition means that word appears in the text of the definition.

… shall not be deemed …

“Shall not” prohibits the action. “To deem X to do Y” means to interpret X as doing Y such that you treat X as doing Y.

… to exclude other things …

“Exclude” here means excluded from the meaning of the definition. We are talking about, and this applies to, definitions that involve some kind of category. For something to be excluded from the meaning of such a definition means that that thing could not have been written into the statute explicitly without changing the effects of the law. For example, 26 USC § 7701(b)(5)(A) excludes an individual who immigrates to the US for employment as a computer programmer at a private company, and explicitly include such an individual would change the effect of the law. “Other things” means any other thing, i.e., anything other than what was already explicitly listed.

… otherwise within the meaning of the term defined.

“Otherwise” means if not for “includes” or “including” followed by a list of things. A thing being within the meaning of the term defined means that the definition found in Title 26 admits that thing, or, if the statutory definition does not “define” the word in the dictionary sense, then the ordinary meaning of the word admits that thing. For example, 26 USC § 7701(c) is a definition of the terms “includes” and “including” as in “a definition contained in this title”. However, this definition merely clarifies and specifies how these words are being used, and does not provide a “real definition” like you can find in the first, second, third, and fourth definitions above. As a result, we interpret “includes” and “including” as having their dictionary definitions (except with the added specificity of meaning).

Taking it all together, “otherwise within the meaning of the term defined” means that if the term’s definition did not use “include” then we would normally interpret the thing as falling under the definition. For example, in the definition “Cats, including black cats, are small carnivorous mammals”, orange cats is “otherwise within the meaning of” cats.

The terms “includes” and “including” when used in a definition contained in this title shall not be deemed to exclude other things otherwise within the meaning of the term defined.

There is no euphemism and virtually no ambiguity here. There is certainly no doublespeak. It plainly means the exact opposite of what SEDM thinks to be the case (that using “include” limits a definition to those things listed). I believe the claim that this definition “really doesn’t say ANYTHING” reflects SEDM’s inability to come up with an argument. That said, there is a second point SEDM makes to try to downplay the devastating 26 USC § 7701(c). Continuing directly from the previous Great IRS Hoax quote:

But, going along with their game, if you are supposed to believe that these words are expansive in nature, how can you explain the definition for “GROSS INCOME” as stated in the Code?

“SEC. 61(a) GENERAL DEFINITION. – Except as otherwise provided in this subtitle, gross income means all income from whatever source derived, including (but not limited to) the following items…” [Emphasis added]

Why did they feel compelled to add “(but not limited to)?” The answer is self-evident: they knew that “including” is a LIMITING term!(p. 547, §3.9.1.8, emphasis in the original)

So, the point is that when the government really wanted to make it open-ended, they added “but not limited to”, because they knew that otherwise they wouldn’t be able to use the definition “expansively”. This does not make sense. If the government believed “but not limited to” was necessary for the “expansive” meaning, they would have included it in the definitions in Title 26 and elsewhere, as they were allegedly trying to create expansive definitions there too. (Actually, 26 USC § 7701(c) does effectively apply “but not limited to” to all definitions in Title 26, but that would require understanding 26 USC § 7701(c) correctly which is a death sentence for SEDM’s argument.) As far as I can tell, SEDM thinks “but not limited to” does grant the government the expansive powers of definition. In reality, of course, nothing can be lawfully inserted via interpretation into a statutory definition unless it already fits (at least within reason) the definition as written. There have been many cases before the Supreme Court and other courts centered on the question of whether a statute applies to a specific situation.

But why does 26 USC § 61 say “but not limited to”? It’s actually pretty easy to see.

Except as otherwise provided in this subtitle, gross income means all income from whatever source derived, including (but not limited to) the following items:

(1) Compensation for services, including fees, commissions, fringe benefits, and similar items;

(2) Gross income derived from business;

(3) Gains derived from dealings in property;

(4) Interest;

(5) Rents;

(6) Royalties;

(7) Dividends;

(8) Annuities;

(9) Income from life insurance and endowment contracts;

(10) Pensions;

(11) Income from discharge of indebtedness;

(12) Distributive share of partnership gross income;

(13) Income in respect of a decedent; and

(14) Income from an interest in an estate or trust.

This list is so extensive that, sans “but not limited to”, it would not be unreasonable to think this list was absolutely comprehensive. Strictly speaking, the use of “including” alone does allow for possible items covered but not listed, however laws are often written to be carefully unambiguous. Using “but not limited to” guarantees there will be no misunderstanding as to how to correctly interpret the comprehensiveness of the list. This is also the justification for 26 USC § 7701(c).

Powers v. Charron

“Includes is a word of limitation. Where a general term in Statute is followed by the word, ‘including’ the primary import of the specific words following the quoted words is to indicate restriction rather than enlargement.

Powers ex re. Covon v. Charron R.I., 135 A. 2nd 38 829, 832 …”[Treasury Decision 3980, Vol. 29, January-December, 1927, pgs. 64 and 65]

(p. 2685, §5.10.6, emphasis in the original)

This quote is a bit strange. First, it does not appear in either Treasury Decision 3980 or Powers v. Charron. The only source for the Treasury Decision I could find is SEDM themselves, who published a scanned excerpt. Pages 64 and 65 do indeed discuss the meaning of “includes”, though not only is the quote missing, but also the text appears to say the opposite. Finally and most strangely, the quote implies that a document published in 1927 cites a case from 1957.

This quote does appear to support SEDM’s position, although it’s not entirely clear what “restriction” and “enlargement” precisely mean. It is also very similar to what Arnold v. Arnold says, which does not support SEDM’s position. We have to look to Powers v. Charron to understand what it’s saying.

“Section 10-300. Abolishment of Agencies. The following offices, departments, boards and commissions of the City government are hereby abolished as of the effective date of this charter: (a) All existing offices, including specifically the office of Mayor, the Board of Aldermen, the Common Council and the School Committee, except ward and city committees of political parties and the Board of Canvassers and Registration. (b) All existing executive or administrative departments, bureaus and divisions. (c) All existing boards and commissions appointed by the Mayor, the Board of Aldermen, the Common Council, and the City Council, or any of them. …”

After carefully considering the language of sec. 10-300 we are of the opinion that the office of building inspector is not included thereunder. While paragraph (a) refers generally to “All existing offices,” the generality of such language is immediately limited by an enumeration of the offices to which it is intended to apply. This language is not to be extended to include other offices not mentioned, unless it otherwise appears from the charter itself that the enumeration of particular offices was not intended to limit the generality of the foregoing language. This is in accord with the well-recognized principle that “General and specific words in a statute which are associated together, and which are capable of an analogous meaning, take color from each other, so that the general words are restricted to a sense analogous to the less general. Under this rule, general terms in a statute may be regarded as limited by subsequent more specific terms.” 50 Am. Jur., Statutes, § 249, p. 244.

This is by far the closest SEDM has come to supporting their assertion that “includes” means “includes only”. Indeed, this decision is contrary to my normal understanding of “including”, which is to say that I would have interpreted the statute as applying to the office of building inspector. (The decision explains the context that makes this interpretation make sense—basically it is a different kind of office than those listed.) Unfortunately, it doesn’t quite work out for SEDM.

The question is whether this decision means that laws like 8 USC § 1101 should be interpreted as saying “includes only”. There are three aspects of this to investigate: the justification that the decision provides, the decision itself, and the way the decision has been used to inform subsequent cases.

Powers v. Charron quotes Volume 50 of American Jurisprudence, a legal encyclopedia. I don’t have access to this book, but I doubt there is any missing context that would affect the interpretation of the quote provided. However, this quote is vague, speaking only of “general and specific words”. It is being used in reference to “includes” in a way that seems to support SEDM, but because this is an extremely general principle being applied to a specific case, we need more insight as to how this should apply to other laws. I will consider American Jurisprudence as tentatively supporting SEDM.

There are a few informative pieces within the decision itself which can help us understand why this principle is being applied in this case. First, notice that the quoted law says “including specifically”, language we have not seen up to this point. The addition of the word “specifically” is significant and should be interpreted as affecting the meaning of “including”. It would not otherwise have been used. That being said, the decision doesn’t say anything about the word “specifically”, but nor does it actually say anything about “includes”. Instead, it refers more vaguely to “the enumeration” in the law, which should be interpreted as relating to the general language as “being included specifically” which is different from “being included” in general. Finally, note that the decision says “unless it otherwise appears … that the enumeration … was not intended to limit the generality of the foregoing language.” This statement is included in order to ensure that the decision is not inappropriately extended to situations in which the language clearly implies the existence of items that are covered by but not listed in a statute. The language in 26 USC § 7701(c) clearly states that definitions in Title 26 are not to be interpreted this way. Moreover, even without explicitly saying what “includes” means, 8 USC § 1101(36) also clearly means not to limit the definition to the listed items. It is clear because the vast, vast majority of people understand “the United States” to include the 50 states. For the statute to be understood differently would require different language.

Finally, interpreting a court’s decision on your own is all well and good, but an authoritative interpretation can be gleaned from how the decision has been cited as precedent in later cases. One example is Morris Friedman & Co. v. United States.

In essence, the basic problem in this case is to determine the meaning of the word “includes” as used in headnote 1. Admittedly, the term by itself is not free from ambiguity. “Includes” has various shades of meaning and has been used both as a term of enlargement and of limitation or restriction. Thus, it may be used to preface an illustrative application of a general class, or in the sense of “also” to add to the general class a species which does not naturally belong to it. Phelps Dodge Corp. v. National Labor Relations Board, 313 U.S. 177, 61 S.Ct. 845, 85 L.Ed. 1271 (1941); Helvering v. Morgan’s, Inc., 293 U.S. 121, 55 S.Ct. 60, 79 L.Ed. 232 (1934); Application of Central Airlines, Inc., 199 Okl. 300, 185 P.2d 919 (1947); Illinois Cent. R. Co. v. Franklin County, 387 Ill. 301, 56 N.E.2d 775 (1944). Or it may be used synonymously with “means” or “comprise” as a word of limitation specifying particularly what belongs to the genus. Montello Salt Co. v. Utah, 221 U.S. 452, 31 S.Ct. 706, 55 L.Ed. 810 (1911);[3] Powers ex rel. Doyon v. Charron, 86 R.I. 411, 135 A.2d 829 (1957); Television Transmission, Inc. v. Public Utilities Commission, 47 Cal.2d 82, 301 P.2d 862 (1956); Blankenship v. Western Union Tel. Co., 161 F.2d 168 (CA4 1947); In re Sheppard’s Estate, 189 App.Div. 370, 179 N.Y.S. 409 (1919).

It is, of course, basic that the Congressional intent is the all important factor in construing a statutory provision. Therefore, the court is duty bound to ascertain the legislative purpose by reference to the context and the legislative history. Illinois Cent. R. Co. v. Franklin County, supra; Brecht Corp. v. United States, 25 CCPA 9, T.D. 48977 (1937).

This lays it out pretty clearly and cites many different cases. There are three ways “includes” or “including” can be used: either as illustrating what the law covers, to expand the law to cover specific things that otherwise might not be considered covered, or to enumerate specifically what the law covers. It is only this last situation that agrees with SEDM, but in order for SEDM’s argument to go through this would have to be the exclusive interpretation of “include”.

Another case, Housing Authority v. Bennett, reiterates this high-level understanding of what “includes” or “including” is used to mean.

The authority’s argument is based on the meaning of a single word in § 5-303, “including,” which is somewhat ambiguous. Although this Court has stated that “[o]rdinarily, the word “including” means comprising by illustration and not by way of limitation,'” State v. Wiegmann, 350 Md. 585, 593, 714 A.2d 841, 845 (1998), quoting Group Health Ass’n v. Blumenthal, 295 Md. 104, 111, 453 A.2d 1198, 1203 (1983), we have also recognized that, “[w]hile ‘include’ or ‘including’ may introduce illustrations of a general term, the words also may signal an expansion in meaning of previous language.” Pacific Indem. v. Interstate Fire & Cas., 302 Md. 383, 396, 488 A.2d 486, 492 (1985).

… It is generally held that the meaning of the words “including” or “includes” depends upon the context and that sometimes they are not words of illustration or enlargement. See Helvering v. Morgan’s, Inc., 293 U.S. 121, 125, 55 S.Ct. 60, 61, 79 L.Ed. 232, 235 (1934) (“It may be admitted that the term ‘includes’ may sometimes be taken as synonymous with ‘means'”); Frame v. Nehls, 452 Mich. 171, 178-179, 550 N.W.2d 739, 742 (1996) (“When used in the text of a statute, the word ‘includes’ can be used as a term of enlargement or of limitation, and the word in and of itself is not determinative of how it is intended to be used”); Premier Products Co. v. Cameron, 240 Or. 123, 125, 400 P.2d 227, 228 (1965) (“How [including] is interpreted depends upon several factors,—context, subject matter, possible legislative intention, etc.”). See also, e.g., Television Transmission v. Public Utilities Comm’n, 47 Cal.2d 82, 85, 301 P.2d 862, 863 (1956); Surowitz v. City of Pontiac, 374 Mich. 597, 132 N.W.2d 628 (1965); State v. Sho-Me Power Co-op., 354 Mo. 892, 191 S.W.2d 971 (1946); Application of Central Airlines, 199 Okla. 300, 185 P.2d 919 (1947); Powers v. Charron, 86 R.I. 411, 135 A.2d 829 (1957); Morris Friedman & Co. v. United States, 69 Cust.Ct. 184, 351 F.Supp. 611 (1972).

This decision specifically says “sometimes they are not words of illustration or enlargement”, in direct contradiction to SEDM’s claim that these are never words of illustration or enlargement.

Specific instances in definitions

So it’s established that SEDM cannot possibly be correct in asserting that “include” is always a term of limitation, but nor is it never a term of limitation. SEDM identifies several specific definitions using “include” in a way that is perceived to be problematic (p. 2685, §5.10.6).

“State” found in 26 U.S.C. §7701(a)(10) and 4 U.S.C. §110

The term “State” shall be construed to include the District of Columbia, where such construction is necessary to carry out provisions of this title.

(26 USC § 7701(a)(10))

Because 26 USC § 7701(c) specifies unambiguously how “include” is to be interpreted here, this cannot be a “limiting” definition.

The term “State” includes any Territory or possession of the United States.

(4 USC § 110(d))

Title 4 does not contain any definition for “includes”. However, 4 USC § 110(a) refers to a definition in Title 26, which suggests 26 USC § 7701(c) is a reasonable interpretation of “includes” in the context of Title 4. In general, words not defined in statutes have their ordinary meaning, which for “includes” is not limiting. To reiterate, if the common meaning of “includes” was the limiting one, then SEDM and others would not have written extensively on this topic, having to explain to people that the definition is limiting.

Also, we are to assume “State” has its ordinary meaning except for what the statute specifies. I mentioned this principle in regards to 26 USC § 7701(c), which does not actually explain what “include” means but rather clarifies what it does not mean. “State”, in the context of the United States, ordinarily refers to one of the 50 states. Nothing about 4 USC § 110(d) contradicts this meaning.

“United States” found in 26 U.S.C. §7701(a)(9)

The term “United States” when used in a geographical sense includes only the States and the District of Columbia.

(26 USC § 7701(a)(9))

There’s no issue with this definition as long as “State” is understood correctly per the following definition (or, in the context of this post, the previous definition). This is, for once, very clearly and unambiguously limiting. The word “only” does the heavy lifting.

“Employee” found in 26 U.S.C. §3401(c) and 26 C.F.R. §31.3401(c)

For purposes of this chapter, the term “employee” includes an officer, employee, or elected official of the United States, a State, or any political subdivision thereof, or the District of Columbia, or any agency or instrumentality of any one or more of the foregoing. The term “employee” also includes an officer of a corporation.

(26 USC § 3401(c))

Again, because this is in Title 26, 26 USC § 7701(c) applies. Just to humor SEDM, it may be elucidating to consider why the list was written into the statute, and whether that reason should make it limited. The reason is because in some statutes, government officials or employees are excluded. See for example 29 USC § 203(e)(2) and 42 USC § 2000e(f). Because this statute might otherwise be interpreted as not including these kinds of employees, it is written in explicitly. This is clearly an “expansive” and not “limiting” definition.

26 CFR § 31.3401(c)-1(a) is just the corresponding definition in the Code of Federal Regulations.

“Person” found in 26 C.F.R. §301.6671-1

For purposes of subchapter B of chapter 68, the term “person” includes an officer or employee of a corporation, or a member or employee of a partnership, who as such officer, employee, or member is under a duty to perform the act in respect of which the violation occurs.

(26 CFR § 301.6671-1(b))

Note that this definition is not making an inclusion for corporations but rather for living humans who hold certain positions. As with the previous discussion, let’s consider why this was added to the statute.

In this case, the purpose is not actually to affect who or what are considered “persons”, but rather to expand who can have liability. Many of the statutes in 26 USC Chapter 68 Subchapter B use phrases like “the responsible person”. 26 CFR § 301.6671-1(b) clarifies that, even if the violation was ostensibly an act of a corporation itself, the employee or officer who caused the corporation to take such action is potentially liable. This is a definition that doesn’t make a lot of sense on its own, but does make sense in the context of how “person” is used in Subchapter B and the kinds of issues that arise with these statutes.

This can be seen in how 26 CFR § 301.6671-1(b) has informed court decisions. See for example Slodov v. United States (1978), Thibodeau v. United States (1987), and Williams v. United States (1991).

Ejusdem generis

This argument relates to one of the specific definitions listed above, but goes into a little more depth, so I wanted to focus on it separately here.

“Ejusdem generis. Of the same kind, class, or nature. In the construction of laws, wills, and other instruments, the “ejusdem generis rule” is, that where general words follow an enumeration of persons or things, by words of a particular and specific meaning, such general words are not to be construed in their widest extent, but are to be held as applying only to persons or things of the same general kind or class as those specifically mentioned. U.S. v. LaBrecque, D.C. N.J., 419 F.Supp. 430, 432. The rule, however, does not necessarily require that the general provision be limited in its scope to the identical things specifically named. Nor does it apply when the context manifests a contrary intention.

Under “ejusdem generis” cannon [sic] of statutory construction, where general words follow the enumeration of particular classes of things, the general words will be construed as applying only to things of the same general class as those enumerated. Campbell v. Board of Dental Examiners, 53 Cal.App.3d. 283, 125 Cal.Rptr. 694, 696.”

[Black’s Law Dictionary, Sixth Edition, p. 517]

So when the word “includes” is used, then anything not specified is presumed excluded by the first rule of statutory construction above “Expressio Unius est exclusio alterius”. The second rule of statutory construction above says that when the word “includes” introduces a list of items, then the list must be presumed to be of the same kind or class. For instance, the definition of “United States” found in Title 8 of the U.S. Code says:

8 U.S.C. Sec. 1101(a)(36): State [Aliens and Nationality]

The term ”State” includes the District of Columbia, Puerto Rico, Guam, and the Virgin Islands of the United States.

The above list of items introduced with the word “includes” in Title 8 of the U.S. Code are federal States or territories, and so this is the “general class” that they all fall into. This definition of “State” is the basis for determining whether a person is born in the “United States” for the purposes of citizenship, as defined in 8 U.S.C. §1101(a)(38) and 8 C.F.R. §215.1(f).

If the act doesn’t specifically identify what is forbidden or “included” and we have to rely not on the law, but some judge or lawyer or politician or a guess to describe what is “included”, then our due process has been violated and our government has thereby instantly been transformed from a government of laws into a government of men. And in this case, it only took the abuse of one word in the English language to do so!

(p. 2687, §5.10.6, emphasis in the original)

First, SEDM has Black’s definition backwards. It is referring to specific words followed by general words, not vice-versa. Using “includes” as in 8 USC § 1101(a)(36) involves a general word (“State”) followed by specific words (individual things that are considered “States”). For example, let’s take a look at the case cited, United States v. LaBrecque.

Count I of the Indictment charges the defendant with violating 18 U.S.C. § 1115, which provides in pertinent part:

Every captain, engineer, pilot, or other person employed on any steamboat or vessel, by whose misconduct, negligence, or inattention to his duties …

Defendant contends that the Government has failed to prove that the defendant was “employed” on the Sadie and Edgar … Defendant’s argument focuses upon the following key words found in the statute: “[e]very captain, engineer, pilot, or other person employed on any steamboat or vessel.” [emphasis added]. It is self-evident that the Sadie and Edgar is a vessel and that the defendant is its captain. Defendant’s argument is that the word “captain” must be interpreted with reference to the words “other person employed.” As so interpreted, defendant submits, it becomes plain that the statute was only intended to reach the conduct of persons employed on vessels engaged in commercial activity. …

Accordingly the court must resolve the issue whether captains of noncommercial pleasure vessels, such as the defendant Cyril E. LaBrecque, are subject to the criminal sanctions set forth in Section 1115. The defendant raises a legitimate question as to the meaning of the words employed in the statute. It is helpful to note two maxims of statutory construction which lend some assistance in the interpretation of the words. The maxim, ejusdem generis, limits general terms, i. e., “other person employed,” which follow specific terms, i. e. “captain, engineer, pilot,” to matters similar to those so specified. United States v. Powell, 423 U.S. 87, 96 S.Ct. 316, 319, 46 L.Ed.2d 228 (1975), citing Gooch v. United States, 297 U.S. 124, 128, 56 S.Ct. 395, 80 L.Ed. 522 (1936). Admittedly this is not the usual case where ejusdem generis is employed to interpret the general term. United States v. Insco, 496 F.2d 204, 206 (5th Cir. 1974). Here the question is not who is an “other person employed”; rather it is whether that term limits the definition of “captain” to captains employed on vessels engaged in commercial activity.

(United States v. LaBrecque (1976), emphasis in the original—italics changed to bold)

Strangely, the case cited in the dictionary definition is “not the usual case”, although this decision does affirm that ejusdem generis applies to specific terms followed by general terms. United States v. Insco is cited as “the usual case”. Here, a question was raised as to whether “any card, pamphlet, circular, poster, dodger, advertisement, writing, or other statement relating to or concerning any person who has publicly declared his intention to seek the office of President” applies to bumper stickers. The court decided that ejusdem generis applies here and the very general “writing or other statement” cannot be expanded to include bumper stickers. (United States v. Insco (1974))

Second, the definition for ejusdem generis states that it “does not necessarily require that the general provision be limited in its scope to the identical things specifically named. Nor does it apply when the context manifests a contrary intention.” SEDM would need the former to be the case for their argument. Instead, this specifically says that ejusdem generis does not limit a definition to only those things listed. Moreover, the intention manifested by the context (being 8 USC § 1101) is that “State” should refer to each of the 50 states.

Finally, the second part of Black’s definition just restates the first part, but we can take a look at the additional cited case Campbell v. Board of Dental Examiners (1975). It turns out that the text in the definition comes almost verbatim not from the decision in Campbell itself, but from a quote within the decision. This quote (and thus the second part of the definition) ultimately comes from Scally v. Pacific Gas Electric Co.

“At the time of the fire involved in this case, section 4161.5 of the Public Resourcess [sic] Code provided in pertinent part as follows:

“‘If any fire originates from the operation or use of any engine, machine, barbecue, incinerator, railroad rolling stock, chimney, or any other device which may kindle a fire, the occurrence of the fire [as a proximate result of such cause] is prima facie evidence of negligence in the maintenance, operation, or use of such engine, machine, barbecue, incinerator, railroad rolling stock, chimney, or other device. . . .'”

The essence of appellants’ contention is that the emphasized portion of the instruction includes electric transmission lines. We disagree.

In interpreting a statute or a part of it, we look first to the legislative intent expressed. In the absence of any manifestation of such intent, we must apply general rules of statutory interpretation.

In the present case no evidence of legislative intent has been presented or found. (10) The rule of construction which governs us is the doctrine of ejusdem generis (also known as Lord Tenterden’s rule) which states that where general words follow the enumeration of particular classes of persons or things, the general words will be construed as applicable only to persons or things of the same general nature or class as those enumerated.

(Scally v. Pacific Gas Electric Co. (1972), emphasis in the original—italics changed to bold)

All of this is to say that ejusdem generis doesn’t really apply. It concerns a different kind of issue. But let’s humor SEDM again and suppose that 8 USC § 1101(a)(36) should be subject to this interpretation. Using the definition SEDM provides, does the correct interpretation mean that the 50 states are not “States”? It doesn’t. The criterion for violation is if interpreting “State” to mean one of the 50 states is “construing it to its wildest extent” (paraphrased). That is not the case, as virtually everyone in the United States understands “State” to refer to states.

Tautological definition

This relates to 26 USC § 7701(c), the absolutely devastating statutory definition of “includes” and “including”, which we have already discussed at length and SEDM had no substantive response for. SEDM tries one more approach here.

[T]he definitions of “includes” and “including” are outright deceptions in their own right. A grammatical approach can be used to demonstrate that these definitions are thinly disguised tautologies. Note, in particular, where the Code states that these terms “shall not be deemed to exclude other things”. This is a double negative. Two negatives make a positive. This phrase, then, is equivalent to saying that the terms “shall be deemed to include other things”. Continuing with this line of reasoning, the definition of “includes” includes “include”, resulting in an obvious tautology.

(p. 1624, §5.2.13.2)

The first problem is that “exclude” is not a negative. Negatives in English are terms like no, not, none, not any, no one, nobody, never, nothing, and neither…nor. Include and exclude are antonyms, or words that have opposite meanings. Like open and close, they both have positive meanings that imply taking certain (opposite) actions.

The second problem is that English is not logical, and it’s not possible to force it to be. In first-order logic we have the Law of Excluded Middle, “P or not P”, which enables the rule of inference called double negation elimination. English does not have the Law of Excluded Middle in general. A double negative does not (always) mean the same thing as a positive, and at the very least, it expresses the meaning in a different way. This is particularly true of antonyms, by which I mean that the negation of a word’s antonym is not necessarily the original word. Consider for example the phrase “not unfriendly”, which does not imply friendly. Put simply, there is an “included middle”. This is not such a strange idea. With positives and negatives in math, which are often used to illustrate the concept of a double negative, “nonnegative” emphatically does not mean “positive”. There is an “included middle” of zero. In this case, not excluding other things does not mean including other things. 26 USC § 7701(c) does not necessitate that there must be “other things” to be included. In other words, when there are no “other things”, we’re not including anything extra but neither are we excluding anything.

The third problem is that the definition of the “includes” including “include” would not make it a tautology. That would make it a circular definition, which in fairness would be a bad definition, but I don’t want to skim over SEDM’s misunderstanding of what a tautology is. While a definition can be read as an indicative statement (“‘To include’ means …”) and thus can be interpreted as a proposition, it is not generally a logical sentence and we don’t normally think of definitions as being true or false, rather accurate or inaccurate. To illustrate the difference for example, “if P and not P then Q” is a tautology. It is always true regardless of the truth values of P and Q. Whether P is true or false, the antecedent is always false, and the material conditional is always true when the antecedent is false (this is why denying the antecedent is a fallacy). Without that logical structure—constituent propositions that can be true or false joined by logical connectives—it’s a little unclear how “tautology” would even work. For additional context, there are statements that are always true in virtue of the meanings of the words and not the logical structure of the sentence, but these are typically referred to as analytic, not tautological. The classic example is “a bachelor is an unmarried man”, which is always true because “bachelor” means “unmarried man”. Note that this is essentially what any definition does if we interpret it as a proposition; every accurate definition is analytic.

There is a second definition of tautology, meaning unnecessary repetition. See for example Merriam-Webster, Cambridge, Collins, etc. and even Black’s. I would be more inclined to call this definition of “include” a tautology if the “positive” version (where “not exclude” is changed to “include”) said that definitions using “include” include what is listed as being included, but that’s not what it says. It says other things (not listed) are included. Since that is not a necessary part of inclusion (under its ordinary meaning or in how it has been used in statutes), it is not redundant to specify.

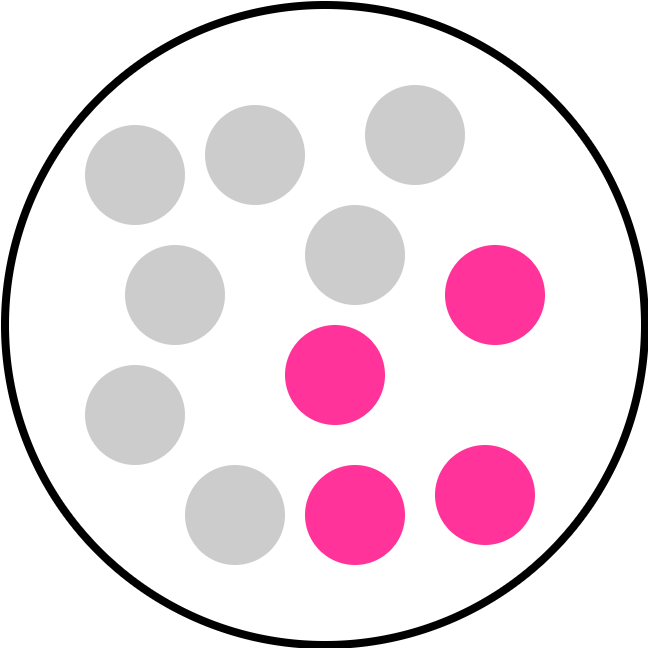

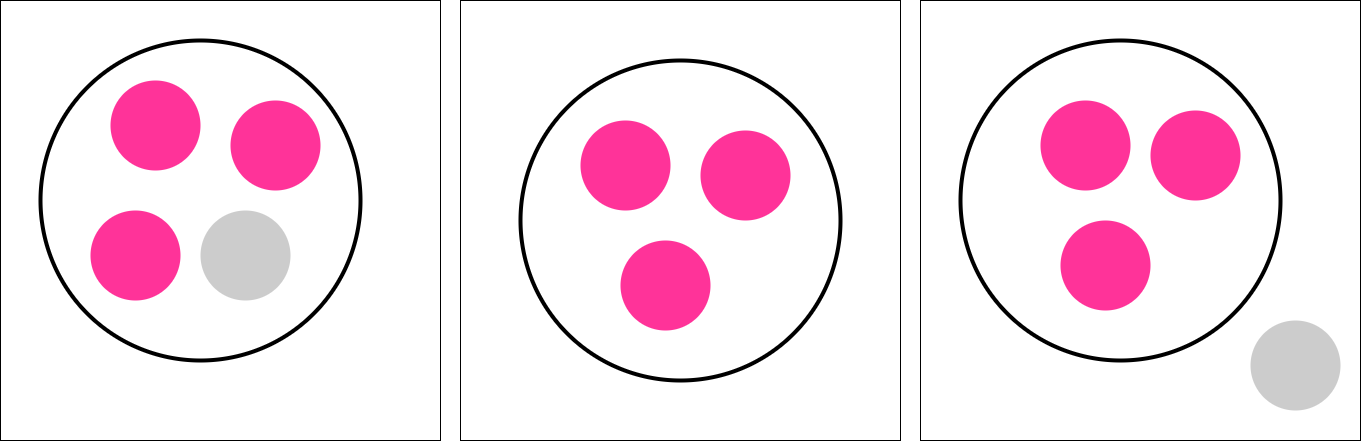

Center: the circle includes pink dots and neither includes nor excludes gray dots.

Right: The circle includes pink dots and excludes gray dots.

Void for vagueness

SEDM repeatedly claims that, if the “expansive” meaning of “include” is used, then such a law is “void for vagueness” (see e.g. p. 485, §3.6.2; p. 535, §3.9; p. 558, §3.9.1.15; p. 1631, §5.2.13.3; p. 1714, §5.3.1; p. 1727, §5.3.3; p. 2679, §5.10.3; p. 2686, §5.10.6; and p. 2897, §6.12.4).

There is a concept called the “void for vagueness” doctrine that was advocated by the U.S. Supreme Court. This doctrine is deeply rooted in our right to due process … A statute must be sufficiently specific and unambiguous in all its terms, in order to define and give adequate notice of the kind of conduct which it forbids.

The essential purpose of the “void for vagueness doctrine” with respect to interpretation of a criminal statute, is to warn individuals of the criminal consequences of their conduct. … Criminal statutes which fail to give due notice that an act has been made criminal before it is done are unconstitutional deprivations of due process of law.

[U.S. v. De Cadena, 105 F.Supp. 202, 204 (1952), emphasis added]

If it fails to indicate with reasonable certainty just what conduct the legislature prohibits, a statute is necessarily void for uncertainty, or “void for vagueness” as the doctrine is called. … Any prosecution which is based upon a vague statute must fail, together with the statute itself. A vague criminal statute is unconstitutional for violating the 5th and 6th Amendments. The U.S. Supreme Court has emphatically agreed:

“That the terms of a penal statute creating a new offense must be sufficiently explicit to inform those who are subject to it what conduct on their part will render them liable to its penalties is a well-recognized requirement, consonant alike with ordinary notions of fair play and the settled rules of law; and a statute which either forbids or requires the doing of an act in terms so vague that men of common intelligence must necessarily guess at its meaning and differ as to its application violates the first essential of due process of law.” [Connally et al. v. General Construction Co., 269 U.S. 385, 391 (1926), emphasis added]

The debate that is currently raging over the correct scope and proper application of the IRC is obvious, empirical proof that men of common intelligence are differing with each other.(p. 2696, §5.10.9, emphasis in the original)

Indeed, as we have seen, “includes” and “including” can be ambiguous and can in general be interpreted in different ways. This is the grain of truth upon which SEDM’s argument is based. However, note that:

- None of the cases we discussed involving the interpretation of “include” ended with the law being struck down on vagueness grounds. These laws required judicial interpretation to understand clearly, it’s true, but they were not so vague as to be void for vagueness. To my knowledge there has never been a case where a law was struck down for a vague use of “include”.

- In the particular statutes SEDM is concerned about here—defining “State”, “United States”, etc.—the word “include” is not being used in a vague way, particularly because of 26 USC § 7701(c) providing clarity as to what it means.

- There is no “debate … currently raging over the correct scope and proper application of [Title 26]”. The vast majority of Americans, and virtually everyone in law, business, finance, or government, agree there is no question that “the United States” always includes the 50 states when used to name a geographical area and that people born in any of the 50 states are US citizens under US jurisdiction.

- These arguments have been presented in court and failed.

SEDM’s argument tested in court

United States v. Love (2022) is a case involving a reader of SEDM who was convicted of possessing, distributing, and producing sexually abusive images of minors. To be absolutely clear, this should not be taken to reflect negatively on SEDM, who cannot control their readership. There is no evidence that Love is associated with SEDM in any way other than visiting the website.

The case itself reads like many sovereign citizen cases; it involves the defendant trying to get rid of his court-appointed lawyer, trying to change his plea, trying to submit frivolous motions, challenging the jurisdiction of the court, and so on. Interestingly I found this document which appears to be appendices to a motion the defendant filed. Love explicitly cites SEDM’s Presumption: Chief Weapon for Unlawfully Enlarging Federal Jurisdiction and also presents the same arguments as SEDM regarding “include” (and regarding other issues).

Below: Appendix B1 of Love’s motion (Love even copies SEDM’s system of putting different numbers of asterisks after “United States” without any reference or explanation as to what this means.)

Love also includes this impassioned plea directed at Justice Roberts (the case was not before the Supreme Court):

I have been sentenced to 90 years by a court without jurisdiction, under the statutory interstate commerce definition. In that time I have seen a tremendous amount of corruption that is deeply entrenched in the criminal justice system on all levels. I have witnessed private corporations blatantly ignore the laws and hire illegal immigrants for slave wages ($2 a day) while regular citizens face possible jail time for the same hiring practices. I have seen judges go against the law and make decisions that reflect their special interests not justice. I realized something was very wrong and have thus dedicated thousands of hours to studying and understanding the law. The corruption that I have encountered has shocked me and led to my decision to petition your True Article III Court for relief.

I send you my petition because in these 22 months I have read hundreds of your opinions and believe you understand the constitutional Commerce Clause more than anyone. I am not asking you to make a decision for or against me or for anyone to admit the truth of what is going on, I can clearly see it with my own eyes, nor am I asking you to make some life changing decision that will effect thousands of people. I am asking you to make a life changing decision that will affect me. Your title contains the the words “Honorable” and “Justice” I am

asking you to do the honorable thing and follow the “Rule of Law” when you make your decision, my life is in your hands, please give me justice. Thank you for your most valuable time. I do very much appreciate it.

Love’s conviction and 90-year sentence were upheld.

Based on what I’ve read from SEDM, I think their response would be (a) that they never promise or guarantee any particular outcome in any particular case, and (b) that Love probably did something incorrectly that just stopped the argument from working, or else the judge was corrupt. It is clear, however, that the courts do not buy this line of reasoning at all.

Summary and conclusion

SEDM presents several pieces of evidence and lines of reasoning to the effect that “includes” or “including” when used in statutes (especially those about taxation) means “includes only“. This is essential for the argument that SEDM’s members are not lawfully subject to the federal income tax and other laws. However, these points made by SEDM are a series of misunderstandings of definitions, misinterpretations of law, and misapplications of precedent. What does become clear is that there is a grain of truth in SEDM’s argument: “including” can be ambiguous and can be limiting. The problem is that it can also be expansive, and the clear purpose of “including” D.C., etc. is to expand and not to limit.

It cannot be denied that SEDM (including the author(s) and contributors) spent a tremendous amount of time and effort to research these ideas and write about them. This is perhaps the thing that is most fascinating to me about conspiracy theories. The people who wrote The Great IRS Hoax are not stupid, nor could it really be said that they are ignorant. Ultimately I don’t think this issue is intellectual but emotional.

“Sovereign citizens” and “sovereignty advocates” feel strongly that they should be able to live their lives how they want, usually describing this as “the right to be left alone”. They evidently resent paying taxes and don’t appreciate most of what the government does. When dealing with the government they may feel like they are being pestered, nitpicked, harassed, or even attacked. They are distrustful of human authority figures. It seems to me that some get frustrated when they can’t understand taxation or law without the relevant expertise despite spending many hours researching it on their own. And, like many who are vaguely on the political right, they see many problems with trends in modern American society and culture.

These are all thoughts and feelings that I think people mostly already have prior to learning about “sovereignty” issues. What the conspiracy theory does (like many conspiracy theories) is provide clear answers to confusing questions, validate the feelings and suspicions of the person, provide a community of likeminded people, establish morally black and white “good guys” and “bad guys”, offer the person the “hobby” of researching and writing about the theory themselves, and so on. Maybe in the future I will write more about how conspiracy theories work in general.

I will be writing more about sovereign citizens and about SEDM in particular. In fact, my plan after my first post was to make another post about the movement generally, but I got off on a tangent about SEDM, and while writing about that got off on a tangent about this issue with “include”.